CLI Falls in Fourth Quarter 2022

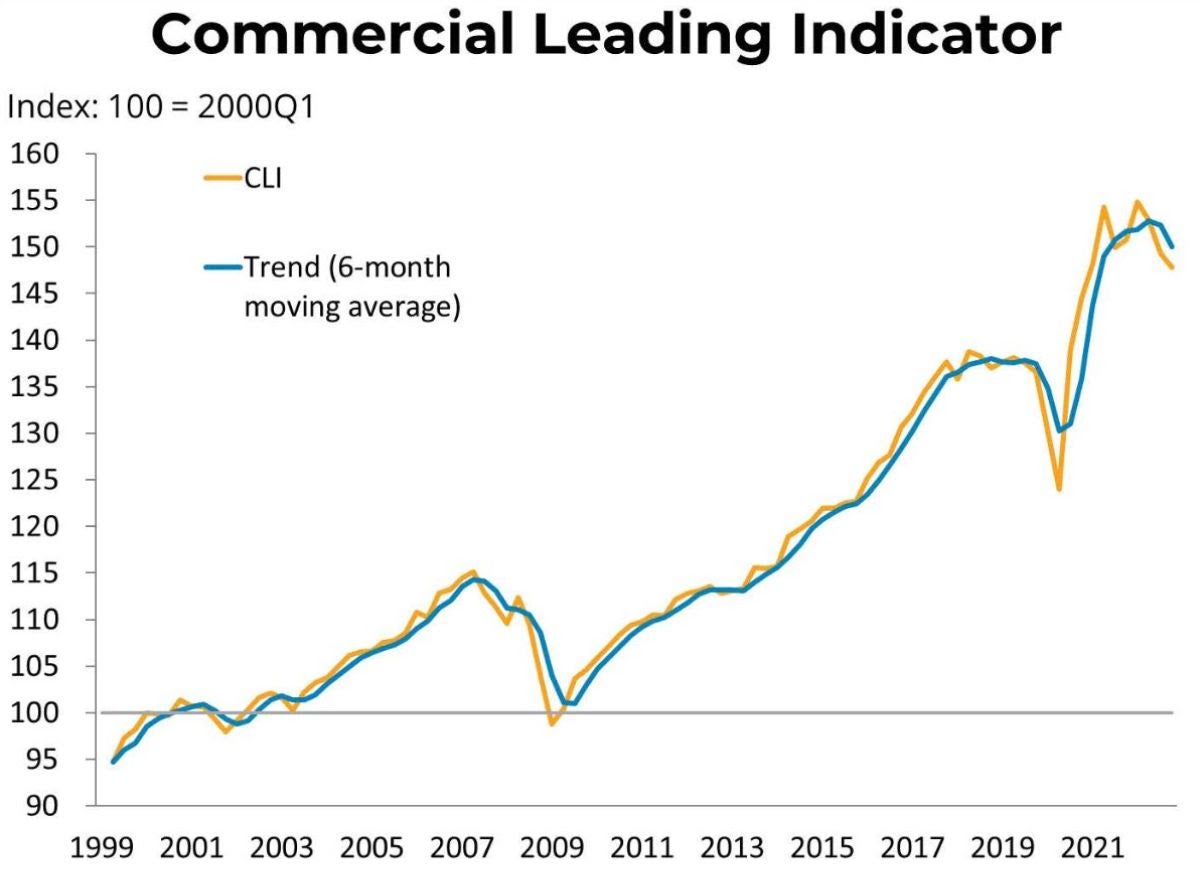

CLI Falls in Fourth Quarter 2022In the fourth quarter of 2022, the BCREA Commercial Leading Indicator (CLI) dropped to 148 from 149, and the six-month moving average continued its downward trajectory. Compared to the same quarter in 2021, the index was down by 2 percent.

It is important to note that the environment for commercial real estate remains highly abnormal and uncertain. The CLI is designed to interpret economic and office employment growth as positive indicators for commercial real estate demand. However, the recent strong growth in these indicators may not translate as readily into improved commercial real estate market conditions due to structural changes in the economy caused by the COVID-19 pandemic.

The decline in the CLI during the fourth quarter was mainly attributed to a deterioration in the economic activity subcomponent of the index.

The economic activity index was driven downwards by inflation-adjusted wholesale trade, retail, and manufacturing sales declines. High inflation has meant that real or inflation-adjusted figures are still negative despite solid nominal growth. The index’s employment component was slightly negative as shrinking office employment (finance, insurance, and real estate) offset rising manufacturing employment. Spreads between corporate and government borrowing costs also rose slightly from the prior quarter, contributing negatively to the financial component. However, rising REIT prices canceled this out, causing the financial component to have zero net effect on the CLI.