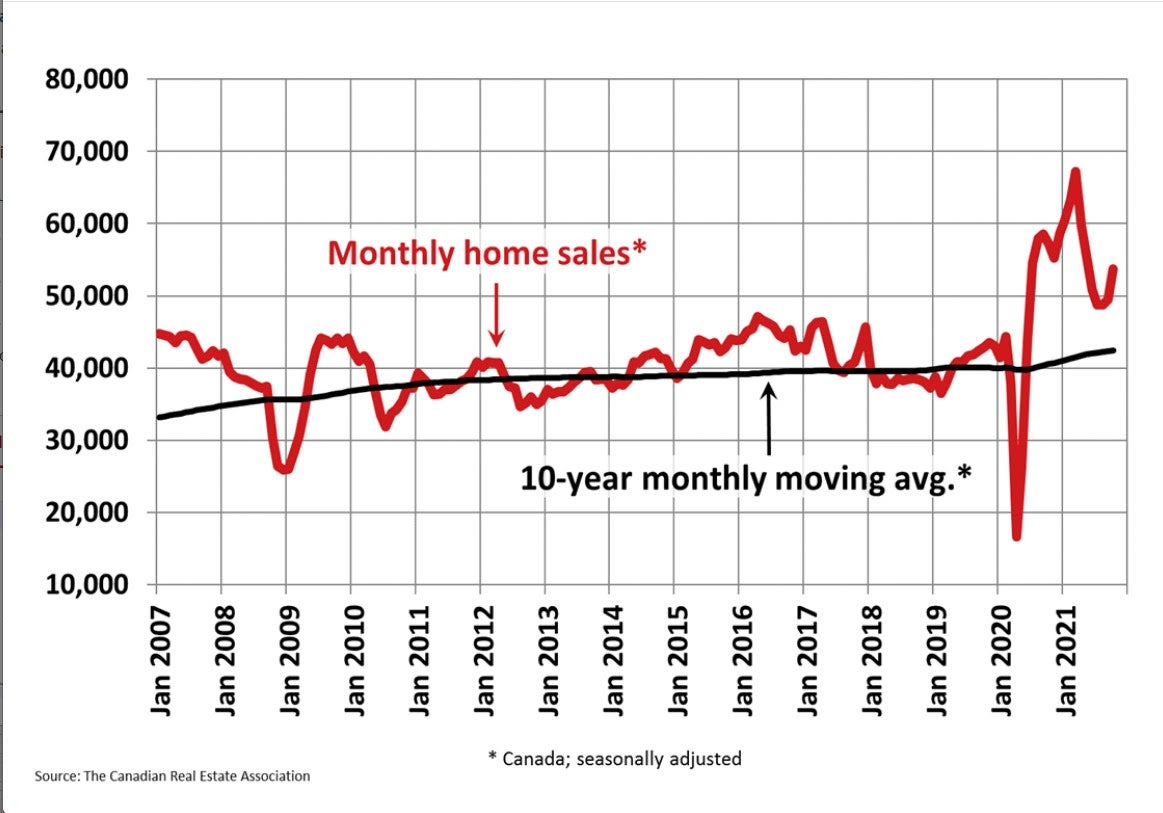

Today the Canadian Real Estate Association (CREA) released statistics showing national existing-home sales rose a whopping 8.6% in October, its most robust month-over-month pace since July 2020, when the first lockdown eased briefly. This was on the heels of a modest uptick in September--the first gain since March of this year.

Today the Canadian Real Estate Association (CREA) released statistics showing national existing-home sales rose a whopping 8.6% in October, its most robust month-over-month pace since July 2020, when the first lockdown eased briefly. This was on the heels of a modest uptick in September--the first gain since March of this year. Sales were up month-over-month in about three-quarters of all local markets and in all major cities.

The actual (not seasonally adjusted) number of transactions in October 2021 was down 11.5% on a year-over-year basis from the record for that month set last year. That said, it was still the second-highest ever October sales figure by a sizeable margin.

On a year-to-date basis, some 581,275 residential properties traded hands via Canadian MLS® Systems from January to October 2021, surpassing the annual record of 552,423 sales for all of 2020.

"2021 continues to surprise. Sales beat last year's annual record by about Thanksgiving weekend, so that was always a lock, but I don't think too many observers would have guessed the monthly trend would be moving up again heading into 2022," said Shaun Cathcart, CREA's Senior Economist. "A month with more new listings is what allows for more sales because those listings are mostly all still getting gobbled up; however, with demand that strong, the supply of homes for sale at any given point in time continues to shrink. It is at its lowest point on record right now, which is why it's not surprising prices are also re-accelerating. We need to build more housing."

The basic story hasn't changed, even with the rise in fixed mortgage rates: Housing demand remains well more than supply. Inventories of unsold properties are at historic lows. While the Trudeau government promised to address the massive supply shortage, in reality, housing construction is under the auspices of provincial and local government planning and zoning bodies. Moreover, the resurgence of immigration will widen the excess demand gap for homes to buy or rent.

New Listings

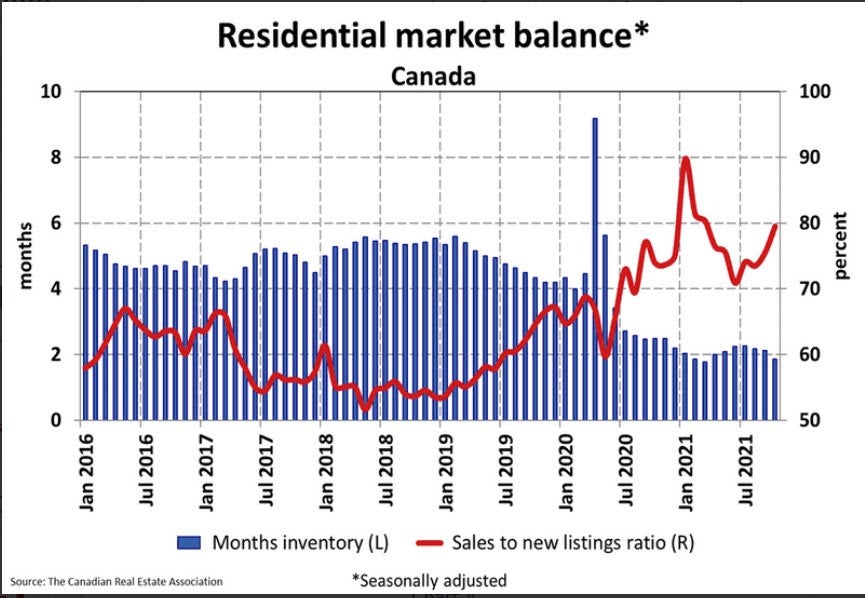

The number of newly listed homes rose by 3.2% in October compared to September, driven by gains in about 70% of local markets. With so many markets starved for supply, it’s not surprising to see sales go up when new listings rise.As of October, about two-thirds of local markets were seller’s markets based on the sales-to-new listings ratio is more than one standard deviation above its long-term mean. The sales-to-new listings ratio tightened again last month to 79.5% compared to 75.5% in September and 73.5% in August. The long-term average for the national sales-to-new listings ratio is 54.8% (see chart below).

There were just 1.9 months of inventory on a national basis at the end of October 2021, down almost half a month from three months earlier and back in line with the all-time lows recorded in February and March of this year. The long-term average for this measure is more than five months.

Home Prices

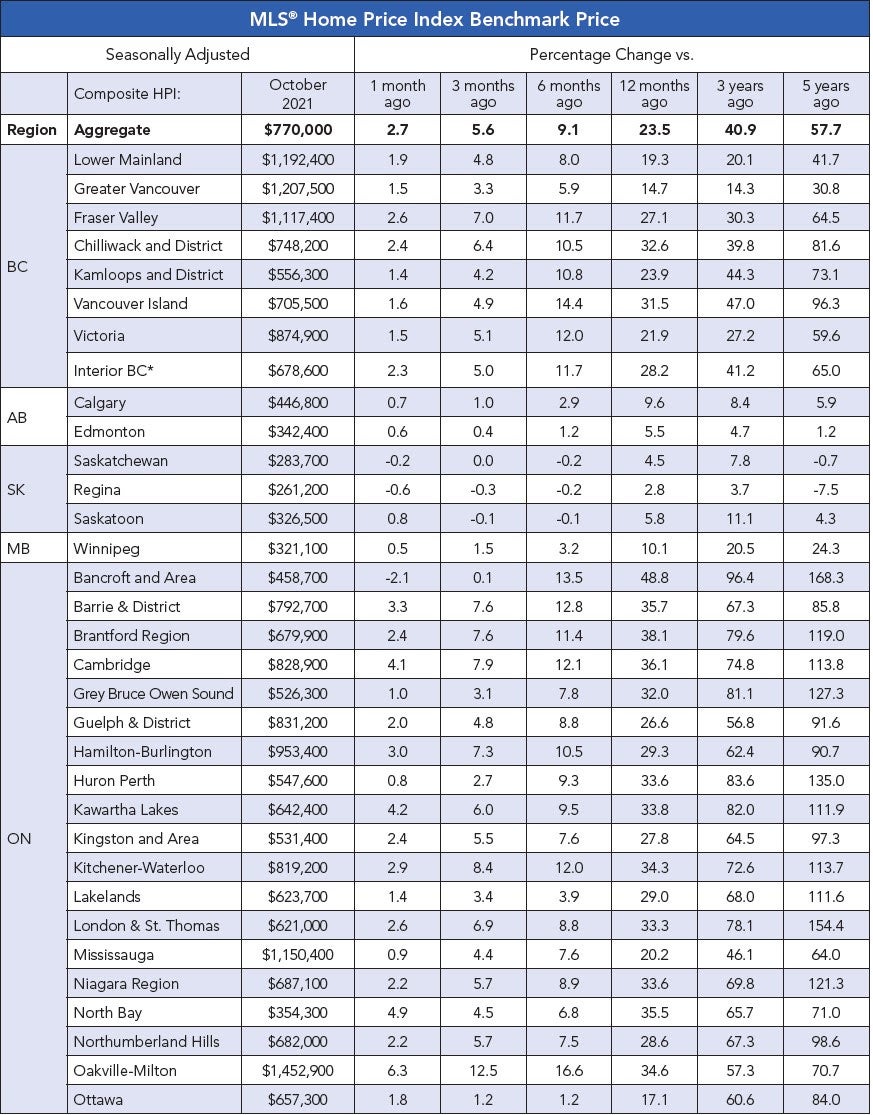

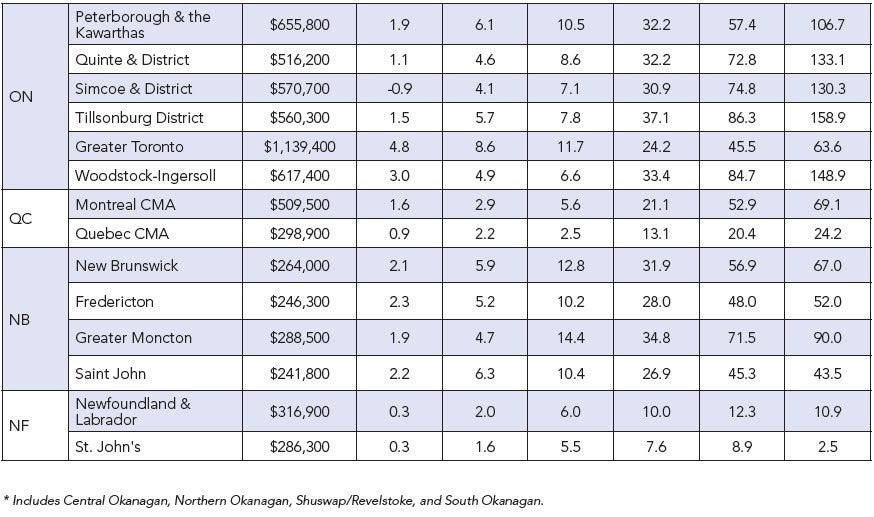

In line with some of the tightest market conditions ever recorded, the Aggregate Composite MLS® Home Price Index (MLS® HPI) accelerated to 2.7% on a month-over-month basis in October 2021.The non-seasonally adjusted Aggregate Composite MLS® HPI was up 23.4% on a year-over-year basis in October, a more significant gain than in the three previous months.

Year-over-year price growth in B.C. has crept back above 20%, though it is lower in Vancouver, on par with the 20% provincial gain in Victoria, and higher in other parts of the province.

Year-over-year price gains are in the mid-to-high single digits in Alberta and Saskatchewan, while they are currently at about 10% in Manitoba.

Ontario saw year-over-year price growth closing in on 30% in October, with GTA surging forward. Greater Montreal’s year-over-year price growth remains at a little over 20%, while Quebec City is now at 13%.

Price growth is running a little above 30% in New Brunswick (a little higher in Greater Moncton, a little lower in Fredericton and Saint John), while Newfoundland and Labrador is now at 10% year-over-year (a bit lower in St. John’s).

Source - DLC - Dr Sherry Cooper